A machine learning framework for solving high-dimensional mean field game and mean field control problems

Abstract

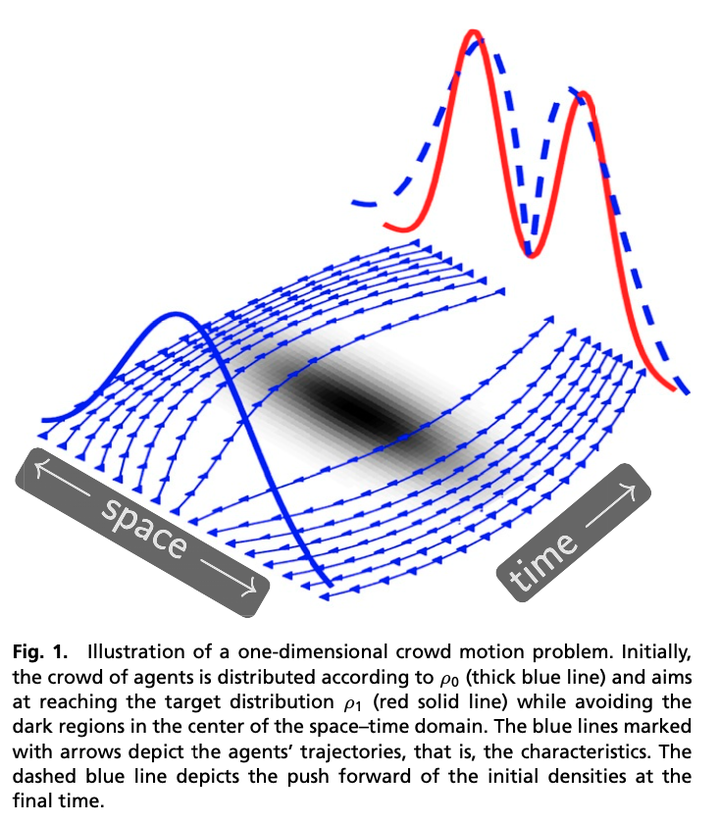

Mean field games (MFG) and mean field control (MFC) are critical classes of multiagent models for the efficient analysis of massive populations of interacting agents. Their areas of application span topics in economics, finance, game theory, industrial engineering, crowd motion, and more. In this paper, we provide a flexible machine learning framework for the numerical solution of potential MFG and MFC models. State-of-the-art numerical methods for solving such problems utilize spatial discretization that leads to a curse of dimensionality. We approximately solve high-dimensional problems by combining Lagrangian and Eulerian viewpoints and leveraging recent advances from machine learning. More precisely, we work with a Lagrangian formulation of the problem and enforce the underlying Hamilton– Jacobi–Bellman (HJB) equation that is derived from the Eulerian formulation. Finally, a tailored neural network parameterization of the MFG/MFC solution helps us avoid any spatial discretization. Our numerical results include the approximate solution of 100-dimensional instances of optimal transport and crowd motion problems on a standard work station and a validation using a Eulerian solver in two dimensions. These results open the door to much-anticipated applications of MFG and MFC models that are beyond reach with existing numerical methods.

Results from the numerical experiments can be downloaded here